I want to apologize in advance for the discouraging, infuriating information I’m about to share. It shouldn’t be hard to use your health insurance to get the addiction treatment your child or other family member needs. But it often is.

When my daughter needed addiction treatment between 2008 and 2012, insurance wouldn’t pay a penny of it. As two entrepreneurs, my husband and I were paying a huge amount for our family’s health insurance on the private market, but treatment for addiction was expressly excluded.

Fortunately, when Obamacare went into effect in 2014, it required that insurance companies cover addiction treatment. (There were other big problems with insurance before Obamacare too. For years, the only policy I could find that covered maternity care at all limited payments to a grand total of $1,000 per pregnancy. What a joke -- it was exhausted before the second trimester even began).

The only silver living of not having any coverage for addiction treatment was that we got to choose where to send Karina for treatment and how long she would stay.

When you ask your health insurance to cover your son or daughter’s treatment, you give up control over three crucial decisions.

1. What treatment center to attend

Your insurance company has contracted with a few treatment centers in your area to provide addiction treatment at a low per diem rate. These rehabs are referred to as being “in network”. If you send your family member to one of these centers, you can usually count on them being able to stay for at least a minimum number of days.

If, however, you want to send your child to a rehab with a better reputation, several things must happen. First, you need to have out-of-network coverage on your health insurance. While this was pretty standard for years (albeit usually requiring you to pay a higher percentage of the bill yourself), many families have had to eliminate this option recently to reduce their insurance premiums.

2. When to start treatment

The second thing you have to do is get approval from your insurance to attend this out-of-network program. You and I both know that when a loved one agrees to go to treatment, you’ve got to get them into treatment immediately. Twenty-four hours later, they may have changed their minds or left the house. But insurance companies sometimes make this difficult to attain.

Years ago, my husband shattered his hip following a bad motorcycle accident and became addicted to opioid pain killers. After 18 months of insisting he couldn’t survive without OxyContin, he finally realized the pills were destroying his motivation and memory, and decided to stop taking them. Cold turkey. Since coming off OxyContin causes severe physical and psychological withdrawal symptoms, medically-supervised detox is highly recommended.

But when I called CareFirst Blue Cross to get approval for him to go to a nearby detox center, I couldn’t get through. Even though it was only 10:00 a.m. on a regular Friday morning, their intake department was closed for the next 72 hours! Apparently in their world, people only realize they need addiction treatment on Mondays through Thursdays. (As you can tell, I’m still furious about this 12 years later).

3. How long to stay in treatment

Finally, even if you get approval for your loved one to attend an out-of-network rehab, insurance may not pay for them to remain there as long as you would like. Many insurance companies will decide that someone is ready to step down to a lower level of care (e.g., move from in-patient round-the-clock residential treatment to some sort of outpatient treatment) after as little as two weeks.

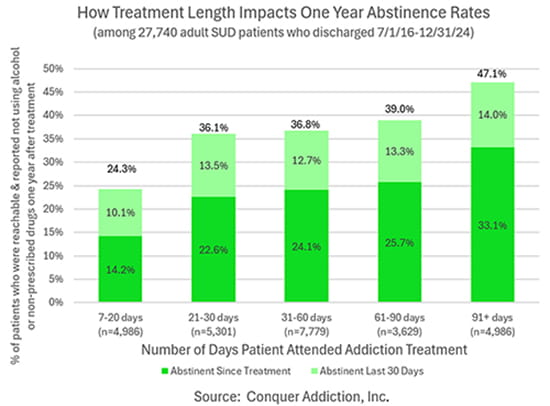

Beware. Our research shows that only about 24% of patients who leave treatment in 20 days or less are doing well one year later:

And, of those we reached who were doing well, 35% had attended additional treatment during the following year.

If you do decide to send your family member to an out-of-network rehab, I recommend that you talk to the admissions team about how many days of covered treatment you can realistically expect, and see if they can give you a discounted cash payment rate should you and the clinical team feel they need to stay in treatment longer.

In summary, when you use your insurance to pay for a family member’s rehab, you may lose the freedom to choose the program they attend, the ability to admit your loved one the moment they finally say “yes,” and the authority to decide how long they stay. None of this is how healthcare should work. But until the system changes, be prepared to advocate fiercely and develop backup plans for foreseeable problems.